FINANCE

Inflation Fatigue Returns to US Households as CPI Climbs to 4.2%

US inflation climbed to 4.2% in May 2026, the highest in three years, with savings at 2.6% and 13% of credit card balances 90 days delinquent.

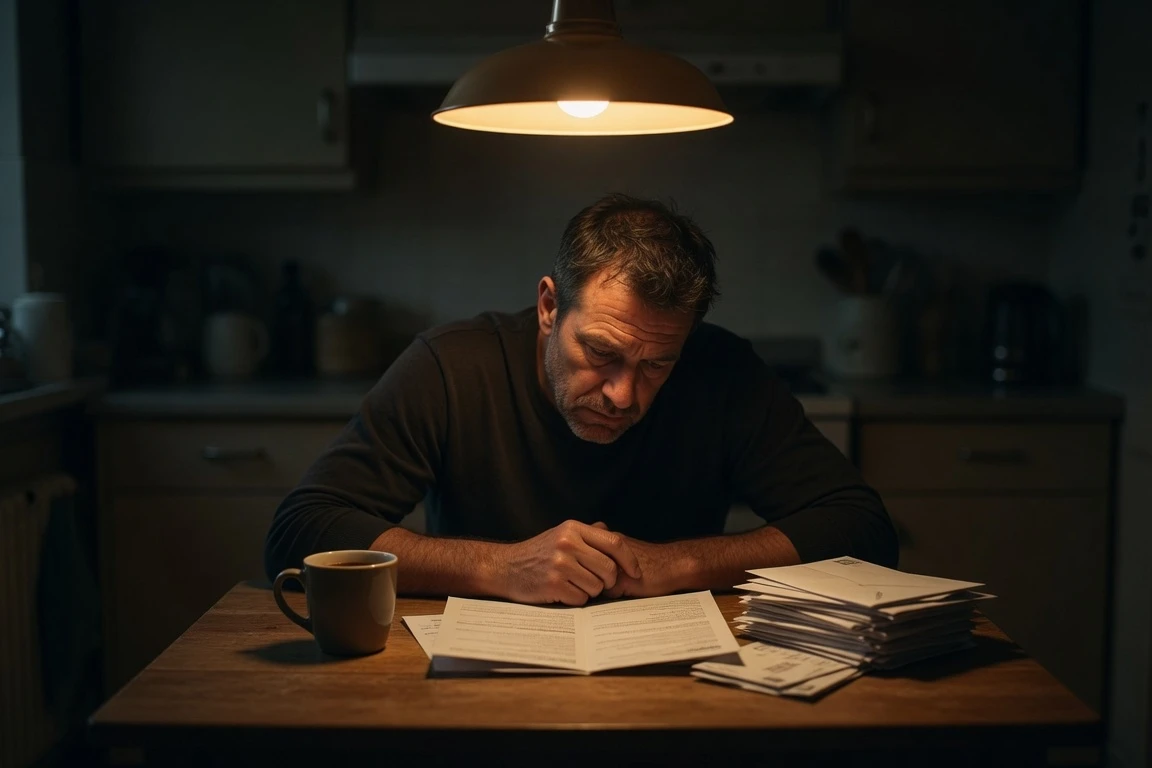

American households are paying more than they did a year ago for almost every essential, and the strain is now visible on credit card balances, in lost sleep, and in the personal savings rate. The US inflation rate climbed to 4.2% over the 12 months ending May 2026, the Bureau of Labor Statistics reported June 10, the highest annual reading since April 2023. Wage growth ran 3.6% in April, before the May acceleration, leaving paychecks losing ground for most of the past year.

That is the backdrop for what economists and the American Psychological Association now call “inflation fatigue,” the condition that hits when consumers grow accustomed to elevated prices that do not come back down. Three years after the worst inflation spike in four decades ended, the bills refuse to fall, and patience is running out.

Inflation Just Hit a Three-Year High Again

The Consumer Price Index climbed 0.5% in May 2026 from the prior month, putting the annual rate at 4.2%, up from 3.8% in April, the Bureau of Labor Statistics reported on June 10. Energy alone accounted for more than 60% of the monthly increase, and gasoline is up 40.5% compared with a year earlier. The core index, which strips out food and energy, rose just 0.2% on the month and 2.9% over the past year, but the headline figure is what households feel when they fill up the tank or pay the electric bill.

Two wage figures tell the rest of the story. Average hourly earnings rose 3.6% from a year earlier in April 2026, already below the 3.8% inflation rate for that month, BLS data show. By May, nominal wages were up 3.82% year on year, still well behind the 4.2% inflation print. Paychecks, in plain terms, are not keeping up with what the same money used to buy.

Heather Long, chief economist at Navy Federal Credit Union, summed up the strain in an email to CNBC. “Americans are getting squeezed financially by inflation that’s back at a 3-year high,” she said, calling out gas, food, electricity, and medical care as “clear pain points that are above 3% inflation.”

| Category | 12-month change through May 2026 |

|---|---|

| All items | 4.2% |

| Energy | 23.5% |

| Gasoline (all types) | 40.5% |

| Food at home | 2.7% |

| Shelter | 3.4% |

| All items less food and energy | 2.9% |

Source: Bureau of Labor Statistics, Consumer Price Index summary released June 10, 2026.

The Iran War Added a Second Wave

The May acceleration did not arrive on its own. The United States has been at war with Iran since early 2026, and oil markets have been repricing around that conflict. “[T]he surge in oil prices could spread to other energy-sensitive parts of the economy,” CNBC reported after the CPI release, noting that energy alone drove the majority of the monthly increase. The national average gas price hit $4.43 a gallon on May 28, 2026, according to AAA data cited by CNBC.

Long called the latest 4.2% reading “a 3-year high” and warned that “the worst is likely still to come for rising food prices,” since fertilizer, transport, and packaging costs ride on energy inputs. The Federal Reserve held its policy rate steady on June 17, 2026, in Kevin Warsh’s first meeting as chair, citing uncertainty tied to the Iran conflict.

Middle-class households already were watching their optimism erode. how middle-class financial optimism has fallen since 2020 shows the long arc of the strain behind this latest reading.

The Savings Cushion Has Collapsed

The personal saving rate, defined as the share of income Americans have after taxes and expenses, fell to 2.6% in April 2026, according to data from the Bureau of Economic Analysis reported by CNBC. A year earlier it stood at 5.8%, almost double. The April reading arrived on May 28, 2026.

Long found the number hard to believe at first. “I thought 2.6% for April was a typo at first. It is so low,” she wrote. “Outside of the revenge spend era of 2022, the personal savings rate has almost never been this low in the past 65 years.”

Americans simply do not have a buffer anymore. A NerdWallet poll of 2,072 adults in early May 2026 found 37% expect to use a credit card, Buy Now Pay Later, or another loan to cover expenses during the month. That included 35% of households earning at least $100,000 a year, evidence the squeeze has climbed past lower incomes.

Credit Cards Are Filling the Gap, and Buckling

Roughly 13% of the nation’s credit card balance was at least 90 days delinquent in the first quarter of 2026, according to the Federal Reserve Bank of New York. The figure has not been that high since 2011, when households were still working through the 2008 financial crisis. The headline 90+ delinquency rate is closing in on the Great Recession peak of 13.7% reached in early 2010.

The average household carries $11,169 in credit card debt, according to WalletHub. The average interest rate on those balances sat at 21% in February 2026, up from 14.6% in February 2022, Bankrate’s 2026 Credit Card Debt Report shows. For cardholders who fall behind, the math compounds quickly: every month of late payments at 21% adds roughly 1.75% to what they owe.

Ted Rossman, principal analyst at Bankrate, sees two Americas inside the data. “[T]here are a lot of people who pay on time, and there are a lot of people who are super-late,” he told USA Today. Heavy delinquencies usually reflect a relatively small share of cardholders with balances they cannot easily repay.

Core price pressure has yet to give the Fed room to step in. why US core inflation has remained above the Fed’s target lays out the data behind that hurdle.

What ‘Inflation Fatigue’ Actually Means

Bankrate defines the term it tracks: “Inflation fatigue happens when consumers grow used to high costs. Instead of changing their spending habits, they have accepted the higher price points.” The American Psychological Association captured the same pattern in March 2022, when 87% of US adults cited “the rise in prices of everyday items due to inflation” as a significant source of stress, the highest reading across any topic since the Stress in America survey began in 2007.

Four years later, the stress has not faded. In June 2026, the American Psychiatric Association found 87% of Americans said they were anxious or very anxious about inflation, up 8 percentage points from a year earlier. The Penny Hoarder survey of 1,000 adults in April 2026 found that 65% said the cost of essential living expenses was their biggest financial worry, and only 14% said they felt in control of their finances.

Many consumers still have enough cash for now, but they will have to belt-tighten later this year as the tax refunds are spent and there isn’t any additional income boost on the horizon for most households.

Heather Long, chief economist at Navy Federal Credit Union, in an email to CNBC, May 28, 2026.

The human costs sit alongside the financial ones. The Penny Hoarder survey found 20% of Americans had delayed medical or dental care in the past three months because of finances, and 23% had increased their alcohol, tobacco, or comfort food consumption. Americans lose an average of three nights of sleep per month to money worries, the same survey reported.

Spending Is Shifting, Not Stopping

The cumulative effect on household spending is selective cuts, not a full stop. According to the Penny Hoarder survey, 42% of Americans skipped a social outing because of money, 23% missed a major family event, and 19% canceled a trip in the past year. Twenty percent reduced or stopped retirement contributions, denting long-term savings for a generation already off pace.

- 37% plan to use a credit card, BNPL, or another loan to cover this month’s expenses

- 42% skipped a social outing to save money in the past year

- 20% reduced or stopped retirement contributions

- 23% increased alcohol, tobacco, or comfort food consumption

- 19% canceled a trip or vacation in the past year

The University of Michigan index of consumer sentiment stood at 49.5 in June 2026 per the final release, up 10.5% from May’s 44.8 but still 18.5% below a year earlier. The fatigue shows in the numbers: even as energy eases slightly, households are bracing for the next reset rather than spending freely again.

What Could Change the Equation

Three forces will decide whether the squeeze eases or tightens from here. Wage growth has to outpace inflation on a sustained basis. The Federal Reserve has to hold or cut rates enough to lower borrowing costs. And the Iran conflict has to settle enough for oil prices to come off their current floor. Long’s view was that Americans want “practical relief, clear information, and a sense that the grind has an end in sight.”

The May reading suggests that end is not yet visible.

Frequently Asked Questions

How high is US inflation right now in 2026?

The Bureau of Labor Statistics reported on June 10, 2026 that the Consumer Price Index rose 4.2% over the 12 months ending in May, the highest annual reading since April 2023. The index climbed 0.5% on the month, up from a 3.8% annual rate in April. Full details are in the May 2026 Consumer Price Index release.

Why is inflation rising again in 2026?

The May 2026 acceleration was driven primarily by energy prices, which jumped 23.5% over the prior 12 months, with gasoline up 40.5%. Oil markets have been repricing around the United States conflict with Iran that began in early 2026.

What is “inflation fatigue”?

Bankrate defines inflation fatigue as what happens when consumers grow used to high costs and accept higher price points without changing spending habits. The American Psychological Association saw the same pattern in its Stress in America survey from March 2022, when 87% of US adults cited inflation as a top stressor.

How low is the US personal savings rate?

The personal saving rate fell to 2.6% in April 2026, according to the Bureau of Economic Analysis as reported by CNBC. A year earlier it stood at 5.8%, almost double. The 2026 Financial Anxiety Barometer findings detail the consumer behavior that follows.

Are credit card delinquencies worse than in 2008?

Not yet, and not across the board. The 13% national credit card balance delinquency rate in Q1 2026 is the highest since 2011 but remains below the 13.7% peak reached in early 2010 during the Great Recession.

Bitcoin Rebounds Past $58K as Warsh Dodges July Fed Rate Question

EquiLibre Lands $500M as Creandum Places Its Largest-Ever Bet

Dwayne Johnson Wants Out of Politics. Takei and Wheaton Won’t Allow It.

Best Picture 2027: Neon’s Coup, the Andrew Scott Roar, and Cannes Carryover

Qonto and Pennylane: Inside French Fintech’s Odd Couple

Judge Refuses to Dismiss 29 States’ Child Safety Lawsuit Against Meta

Apple’s Hide My Email Has Been Leaking Real Addresses for Over a Year

Common Path Wagers on Social Mobility in UK Startup Hiring

Wayve Opens $85M Employee Tender Offer at $8.6B Valuation

Lenovo’s Legion Y700 Infinite Adds OLED and 5G to the Gaming Tablet

Zcash Patched a Double-Spend Bug as ZEC Climbed 5%

Steam Summer Sale 2026 Locks In June 25 to July 9 Dates

Amazon Scraps Its Stargate Revival After a 20-Week Writers Room

Citigroup Says ETF Outflows Drove Bitcoin’s Crash, Not Strategy’s Sale

CLARITY Act Floor Vote Likely Shifts to August, Lummis Says

Coinbase Invests in Ethena, ENA Jumps 10% on Open-Market Buy

Gigaton Lands $26M to Replace Heavy Industry’s Control Stack

Quobly’s €115M Bet to Scale Silicon Quantum Computing

Coinbase for Agents Lets AI Trade and Spend From Your Account

Why DORA and NIS2 Make Vendor Risk a Daily Job in Europe

-

FINANCE4 weeks ago

Zcash Patched a Double-Spend Bug as ZEC Climbed 5%

-

ENTERTAINMENT4 weeks ago

Steam Summer Sale 2026 Locks In June 25 to July 9 Dates

-

NEWS2 months ago

NEWS2 months agoMeta Adds AI Replies to Threads, But Users Can’t Block It

-

ENTERTAINMENT1 month ago

ENTERTAINMENT1 month ago‘Widow’s Bay’ Review: Apple TV’s Sleeper Horror-Comedy Earns Its Fog

-

ENTERTAINMENT4 weeks ago

Amazon Scraps Its Stargate Revival After a 20-Week Writers Room

-

FINANCE4 weeks ago

Citigroup Says ETF Outflows Drove Bitcoin’s Crash, Not Strategy’s Sale

-

FINANCE4 weeks ago

CLARITY Act Floor Vote Likely Shifts to August, Lummis Says

-

FINANCE4 weeks ago

Coinbase Invests in Ethena, ENA Jumps 10% on Open-Market Buy